Every Arizona driver is legally required to carry auto insurance, and understanding Arizona auto insurance requirements is essential for protecting your rights, finances, and driving privileges. Whether you’re a longtime Arizona resident or just moved to the state, knowing the ins and outs of these laws ensures your commute to work every day is protected.

At Shapiro Law Team, we’ve helped residents protect their legal rights while making sure they have proper insurance coverage. Our comprehensive guide will cover the basics of Arizona auto insurance requirements, the importance of proper compliance, and how to select the right insurance policy for your specific situation.

An Overview of Arizona Auto Insurance Laws

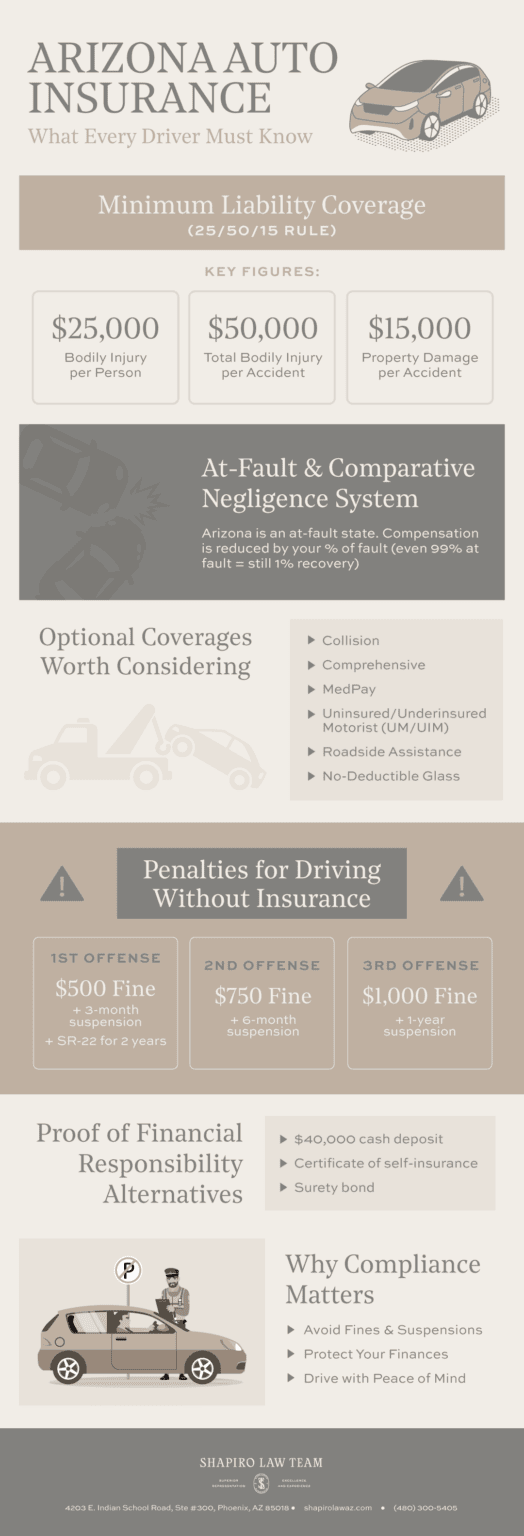

Arizona operates under an at-fault insurance system, meaning the driver who causes an accident is financially responsible for the resulting damages. Unlike no-fault states, Arizona drivers file claims through the at-fault driver’s insurance company rather than their own.

Additionally, Arizona follows the principle of pure comparative negligence. This means that each party involved in an accident may be assigned a percentage of fault, and their compensation is reduced by that percentage.

For example, if you’re found to be 20% at fault in a crash, any damages awarded to you would be reduced by 20%.

In addition, all drivers must carry proof of financial responsibility at all times, which typically means showing a valid auto insurance card. However, other alternatives, such as deposits or certificates of self-insurance, are available under state law.

Arizona car insurance laws also mandate that insurance coverage is in place not just for operating a vehicle, but also for registering it. Failing to maintain continuous coverage can result in penalties, even if your car isn’t being driven.

Minimum Liability Auto Insurance Requirements in Arizona

In Arizona, state law requires drivers to carry minimum liability insurance to operate a motor vehicle legally. These coverage limits are sometimes referred to as “25/50/15” and include the following:

- $25,000 for bodily injury or death per person

- $50,000 for total bodily injury or death per accident

- $15,000 for property damage per accident

This means if you’re responsible for a crash, your policy must be able to pay up to $25,000 for injuries to one person, $50,000 total if multiple people are hurt, and $15,000 for damage to someone else’s property.

These insurance minimums apply to all registered vehicles, including cars, trucks, motorcycles, and mopeds. Failure to meet these requirements can trigger immediate consequences from the Arizona Department of Transportation (ADOT).

Understanding Arizona Liability Insurance

In Arizona, liability insurance pays for injuries and property damage you cause to others in an accident where you’re found at fault. It doesn’t cover your own medical bills or vehicle repairs.

Here are some examples of how this works in practice:

- If you rear-end someone at a stoplight, your bodily injury liability helps pay for their emergency room visit and follow-up care.

- If you sideswipe a car while changing lanes, your property damage liability helps cover their repair costs.

- If multiple people are injured in a single crash you caused, your insurance covers the victims up to the policy limits (e.g., $50,000 per accident).

Liability coverage for both bodily injury and property damage is required by Arizona law, but it’s often not enough to cover serious accidents. That’s where optional coverages can help fill in the gaps.

Optional Insurance Coverages for Arizona Drivers

Arizona drivers aren’t required to carry more than liability coverage, but many choose to add extra protection. Optional insurance plans offer financial safety nets when basic liability limits fall short.

Here are some of the most common optional coverages:

- Comprehensive Coverage: Covers non-collision damage like theft, vandalism, hail, or fire.

- Collision Coverage: Pays for repairs to your own car if you’re at fault in an accident.

- Medical Payments Coverage (MedPay): Covers your own medical bills regardless of fault.

- Uninsured/Underinsured Motorist Coverage (UM/UIM): Protects you if you’re hit by a driver with no insurance or insufficient coverage.

- Gap Insurance: Covers the difference between what you owe on a loan/lease and your car’s value if totaled.

- Roadside Assistance: Helps with towing, lockouts, jumpstarts, or flat tires.

- Accident Forgiveness: Prevents your rates from rising after your first at-fault accident.

- No-Deductible Glass Coverage: A unique perk for Arizona drivers, this option covers windshield repair/replacement with no out-of-pocket costs.

Penalties for Driving Without Insurance in Arizona

Driving without insurance is considered a serious offense in Arizona, and the penalties range from a license suspension to paying fines. During the suspension period, you won’t be able to legally drive or register any vehicle in your name.

Reinstating your license requires paying fines, obtaining SR-22 insurance, and possibly completing traffic courses.

The penalties also escalate with each violation:

First Offense

- Fine: $500

- License & Registration Suspension: 3 months

- SR-22 Certificate: Required for 2 years to prove future financial responsibility

Second Offense

- Fine: $750

- License & Registration Suspension: 6 months

- SR-22: Still required

Third or Subsequent Offense

- Fine: $1,000

- License & Registration Suspension: 1 year

- SR-22: Still required

Comparative Negligence and Fault Laws in Arizona

Arizona follows a pure comparative negligence system. This means that each party in an accident can be assigned a percentage of fault, and their compensation is reduced accordingly.

For example, if you’re 10% at fault for an accident and the other driver is 90% at fault, you can still recover damages. However, your award will be reduced by 10%. Even if you’re 99% responsible, you can still claim 1% of the damages.

This system adds complexity to insurance claims and lawsuits, especially when fault is disputed. Working with a Phoenix car accident lawyer can help protect your rights and ensure your percentage of fault is fairly assigned.

Diminished Value Claims in Arizona

Even if your vehicle is fully repaired, it may still lose resale value after a car accident. That loss is known as diminished value, and Arizona drivers may be eligible to file a claim for it.

A diminished value claim allows you to recover the difference between what your car was worth before the accident and what it’s worth after repairs. You can file a diminished value claim if:

- You were not at fault in the accident

- Your vehicle sustained significant damage and was repaired

- The other driver’s insurance company accepted liability

While not all insurers are quick to pay these claims, Arizona does not prohibit them, and many drivers receive fair compensation when they provide detailed documentation.

Arizona’s Mandatory Insurance Law: What It Legally Requires

Arizona Revised Statute (ARS) § 28-4009 outlines the state’s mandatory insurance law for motor vehicles. It also defines allowable exclusions, such as intentional acts or drivers excluded from the policy by name.

The key Arizona auto insurance requirements include:

- All Arizona-registered vehicles must have a motor vehicle liability policy

- Minimum coverage limits are 25/50/15

- Policies must be issued by a company authorized to do business in Arizona

- Coverage must be continuous, even for vehicles not in daily use

Proof of Financial Responsibility Alternatives

While most people comply with Arizona’s insurance law by purchasing a standard policy, there are alternative options available. These alternatives require approval and often involve additional paperwork and legal oversight. They’re typically used by businesses, not individual drivers.

Acceptable alternatives for proof of financial responsibility include:

- $40,000 cash deposit with the Arizona Office of the Treasurer

- Certificate of self-insurance for fleet owners or large companies

- Surety bonds or partial deposits under specific conditions

Arizona Auto Insurance for New Residents

If you’re moving to Arizona, you’ll need to update your insurance and registration fairly quickly.

Once you’ve finished unpacking your boxes, you must:

- Obtain an Arizona auto insurance policy before registering your vehicle.

- Transfer your vehicle registration within 15 days of establishing residency.

Your existing out-of-state policy may not meet Arizona’s liability minimums, so be sure to check with your insurer.

Arizona’s desert driving conditions, wildlife hazards, and open highways may also affect the type of coverage you need, especially for windshield repairs or roadside assistance.

Tips for Choosing the Right Insurance Policy in Arizona

Meeting Arizona’s minimum insurance requirements is just the start. Choosing the right policy means tailoring your coverage to match your vehicle, lifestyle, and local driving conditions.

When shopping for Arizona liability insurance, follow these tips to help you choose the right one:

Consider Your Needs Beyond State Minimums

Minimum liability limits might not cover the cost of serious accidents or multiple injuries. Adding comprehensive, collision, and uninsured motorist protection can reduce risk, especially if you drive frequently or live in high-traffic areas.

Compare Quotes and Company Ratings

Premiums can vary dramatically between insurers. Use comparison tools to review monthly or annual rates, customer satisfaction ratings, and claim response times.

Consider Arizona’s Unique Driving Conditions

From desert dust storms to cracked windshields and monsoon flooding, Arizona’s environment can impact your insurance decisions. No-deductible glass coverage is beneficial due to the frequent windshield damage caused by sand and gravel. Roadside assistance can also be particularly valuable in rural or mountainous areas.

Why Compliance with Arizona Insurance Laws Matters

Failing to comply with Arizona’s car insurance requirements can lead to more than just a traffic ticket. It can affect your driver’s license, registration, financial future, and even your ability to recover damages in an accident.

When you stay compliant with Arizona auto insurance requirements, you:

- Avoid Legal Penalties: Arizona imposes steep fines and license suspensions for uninsured drivers.

- Protect Your Finances: Accidents can cost thousands, and adequate coverage ensures you’re not paying out of pocket.

- Have Peace of Mind: Knowing your policy meets state requirements lets you drive with confidence.

- Gain Better Claim Outcomes: Drivers who maintain good coverage and keep their records clean often see lower premiums and better support after accidents.

Need Legal Help After a Car Accident?

Understanding Arizona car insurance laws is one thing, and navigating an accident claim is another. If you’ve been hit by an uninsured driver, are facing penalties for a lapse in coverage, or need help disputing fault in a crash, you don’t have to go it alone.

Reach out to our team of licensed Phoenix car accident lawyers at Shapiro Law Team for legal support and guidance that protects your rights. Our team works on a contingency fee basis, meaning you don’t pay us a thing unless we win your case.

Frequently Asked Questions

Is full coverage required in Arizona?

No. Arizona only requires liability insurance that meets the 25/50/15 minimums. However, full coverage is strongly recommended for newer vehicles or financed cars.

Can I reject uninsured motorist coverage?

Yes. UM/UIM coverage is optional in Arizona. However, insurers are required to offer it to you, and if you reject it, you must do so in writing.

What happens if an uninsured driver hits me?

If you don’t have UM coverage, you might be forced to pay for damages out of pocket. You can also sue the at-fault driver, which can be difficult if they lack assets. UM/UIM coverage provides peace of mind in these situations.

What are Arizona’s laws on teenage drivers and insurance?

Teen drivers must be insured under a liability policy, either their own or their parents’. Insurance premiums are typically higher for young drivers, so families often shop around to find affordable options with good coverage.